Why This 27-Year-Old Professional Used VUL to Achieve His Goal of FIRE

How permanent life insurance gave this high earner a head start on achieving financial independence and retiring early

Starting early is one of the most powerful advantages when building long-term wealth, and many advisors can cement multigenerational relationships by understanding different strategies unlocked by permanent life insurance. The trick is beginning earlier than most people think, before the client might even be thinking about building a family. When working with high-earning professionals who have maxed out their traditional retirement vehicles or exceed salary limitations, advisors should consider the tax-advantaged wealth accumulation option of Variable Universal Life (VUL) insurance. Where a personal savings account acts as emergency savings, a VUL policy can function as a “power” savings account. Let’s walk through how a tailored VUL policy balances risk and reward, and creates a supercharged savings account.

Background: Setting the Stage for Future Success

Let’s use Harvey as an example: a 27-year-old male and part of the HENRY demographic—High Earners, Not Rich Yet. He approached his advisor with a healthy savings habit, but felt he had yet to exhaust his options of tax-advantaged wealth vehicles that could work towards his goal of building the most retirement income. As a self-proclaimed member of the FIRE movement, Harvey was prepared to save as much as possible so that he could create financial independence and retire early.

Harvey’s goals included:

Building tax-advantaged retirement income

Embracing risk through market exposure

Maintaining flexibility for when he started a family

The Solution: Risk-Tolerant Growth with Built-In Flexibility

After his advisor reviewed his portfolio and risk appetite, he leveraged the Optifino platform to identify the perfect product for his client’s goals: a Variable Universal Life (VUL) policy. The VUL policy provided market exposure and a reliable pathway for growth, insulating against capital gains as he invested in the market within the policy.

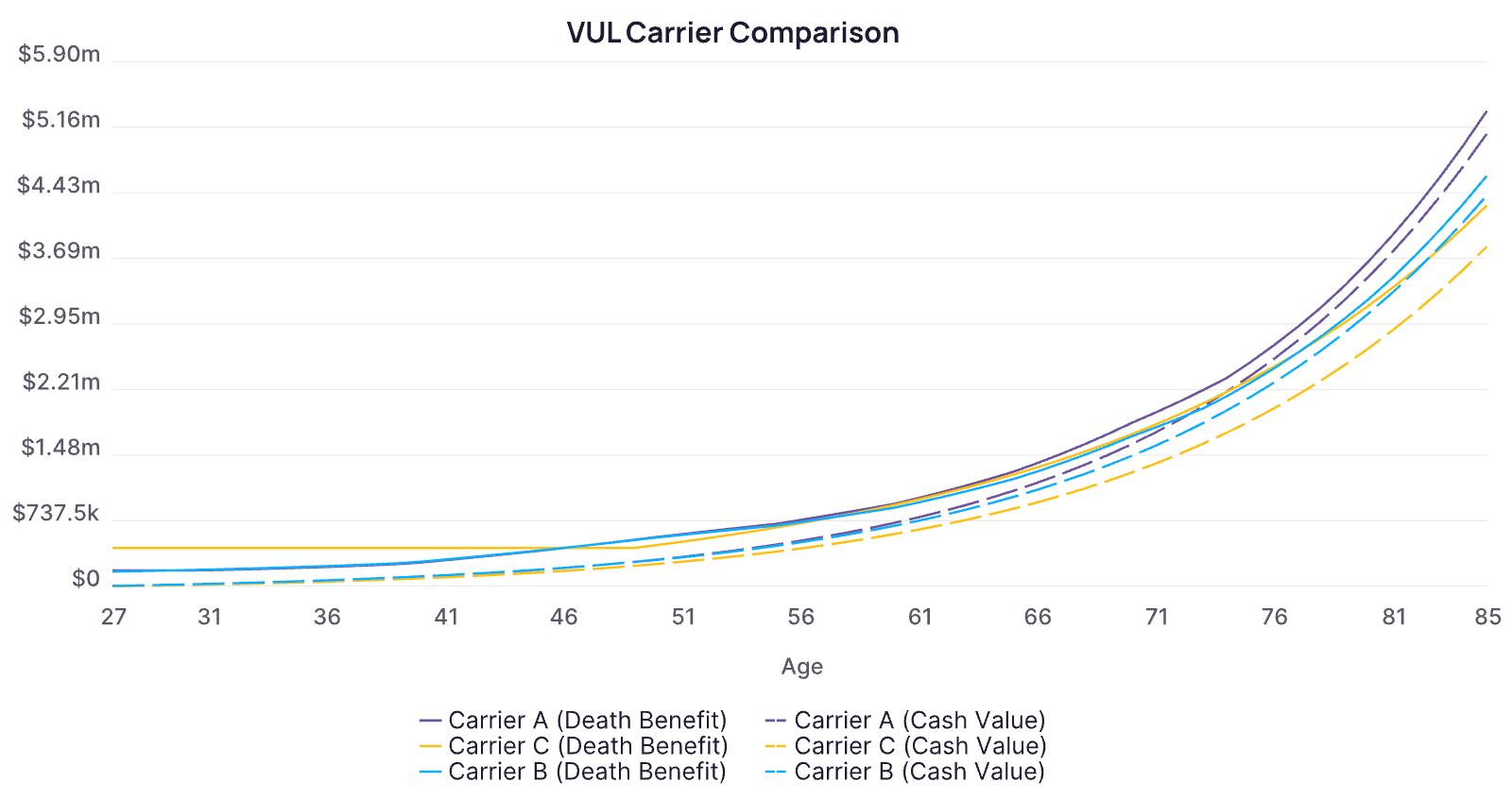

This graph compares VUL policies from three of the industry’s most reputable carriers, and illustrates how Carrier A offered the highest Death Benefit and Cash Value among the options. For a $5K annual premium, Harvey was able to secure:

Initial Death Benefit: $5M at life expectancy (assuming 8% return)

Projected Cash Value at Age 65: $1M (assuming 8% return)

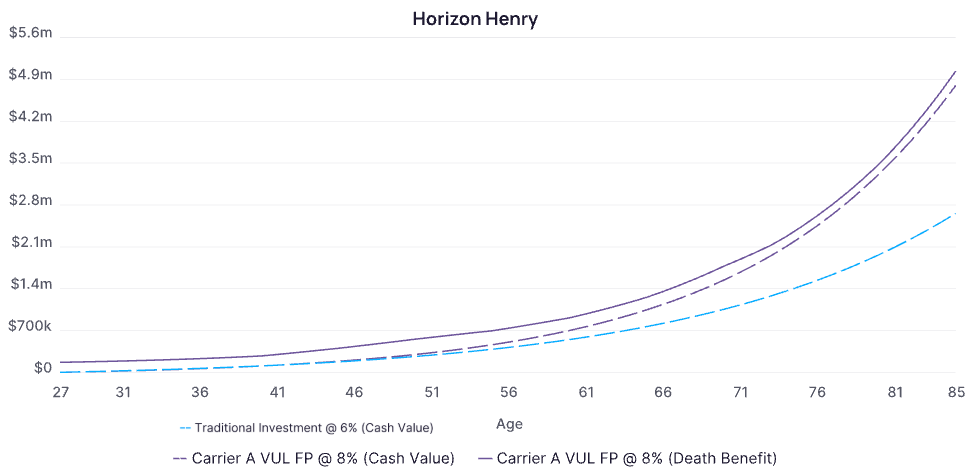

The graph above compares the projected performance of Harvey’s Variable Universal Life (VUL) policy to a traditional investment account—highlighting the tax draft of long-term capital gains tax on a traditional investment account. The tax-free accessibility of the VUL policy means that the cash value grows to $1,071,389 by age 65, while a traditional investment would only yield $768,807 in accessible income because of the 25% tax drag. While both options offer market exposure, the VUL adds a key advantage: tax-deferred growth, tax-free access via policy loans, and a a tax-free death benefit.

Closing Thoughts

Harvey’s story is a great example of how the right life insurance strategy isn’t just about protection—it’s about potential. Advisors can help their clients start optimizing for long-term goals sooner than many believe, creating trust early in the relationship that they are developing the most holistic strategy. By starting early, the client is also able to minimize the cost of insurance, and maintain their health status later on should they decide to convert to a more protection-oriented policy. Our platform empowers the advisor to make the optimal policy recommendations in minutes—no longer taking days to shop around with each carrier and create analog projections. At Optifino, we empower advisors to identify the perfect policy to contribute to their client goals, no matter the life stage.