The Power of VUL: Embracing Risk with Tax Advantages

Think of it as a tax wrapper around an ETF. The power of compounding money tax advantaged over time.

If Risk is a Financial Priority

Every day, we speak to people who think that life insurance is only useful for its protective properties. Too many do not understand how life insurance can be used to build wealth and instead put their money toward other less tax-advantaged financial vehicles. In fact, the leading reasons for not having life insurance or not having enough coverage is the belief that it’s too expensive, that it gets in the way of other financial priorities, and that they do not know how much or what type to buy (LIMRA). The reality is that costs vary by as much as 40% across carriers, and can also vary widely across different products. Depending on your budget and risk tolerance, there are a few types of life insurance policies that enable people to be more risk-tolerant (e.g. PPLI, VUL). We will explore how VUL unlocks the ability to create tax-efficient market exposure, and can be utilized as a tax-advantaged strategy to accumulate wealth while providing coverage.

Understanding Variable Universal Life (VUL) Insurance

Variable Universal Life (VUL) Insurance is a dynamic financial product that merges the long-term protection of life insurance with the flexibility of investment options. This unique blend allows policyholders to adjust their premiums and leverage a cash value component, accessible during their lifetime. The cash value in VUL policies is invested in various subaccounts resembling mutual funds, presenting an opportunity for significant growth. However, it's important to note that this potential comes with exposure to market risks, which could lead to substantial gains and losses.

The allure of VUL lies in its tax-efficient features. Growth within the policy's cash value is tax-deferred, providing a strategic advantage for policyholders. Access to this cash value is facilitated through taxable withdrawals or tax-free loans, offering a flexible approach to financial planning.

Tax Implications Explained

The beneficiary inherits the death benefit tax-free. The tax treatment of VUL insurance policies is guided by Section 101(a)(1) of the tax code, which essentially exempts amounts received from a life insurance contract due to the insured's death from being counted as gross income. For further details, you can refer to the IRS document here: IRS Document RR-07-13.

The policyholder may borrow against the value tax-free. A significant benefit of VUL policies is the ability to borrow or withdraw (up to your basis) from the cash value tax-free, using the policy's death benefit as a repayment mechanism. This strategy allows for the cash value to potentially grow unimpeded by taxes, enhancing the policy's value over time. Generally, borrowing costs are minimal (often zero), likened to liquidating stock assets without the associated tax burden.

Is VUL the right policy type for you?

If you're diligently maximizing your contributions to qualified retirement accounts and are on the lookout for additional channels to enhance your retirement savings, VUL insurance is an intriguing option. It not only provides the opportunity to grow your savings in a tax-advantaged setting, but also ensures you benefit from the security of lifelong insurance coverage.

As you embark on the VUL journey, it's crucial to evaluate both the potential rewards and the risks linked to market exposure. Consulting with Optifino and a financial advisor is recommended to ensure that a VUL policy aligns seamlessly with your broader financial goals and strategy.

Understanding the Costs of VUL

The costs associated with a Variable Universal Life (VUL) policy can be multifaceted, reflecting the complex interplay between insurance protection and investment potential. To demystify these expenses, let's break them down:

For example, let's look at a Female, preferred plus, 7 pay policy at $100k / year (Total premium = $700k) where the underlying asset yields 8%.

The purple dashed line = death benefit, the purple solid line = cash value and the blue line represents a traditional 8% return.

Long-Term Value and Costs

Consider the scenario (above) over a 40-year period for a policy projecting an 8% return. The Internal Rate of Return (IRR) on the death benefit might land at approximately 7.58%. This implies that the effective cost for the tax-advantaged nature of a VUL, assuming a lifespan up to 85 years, is roughly 40 basis points.

Cost of Insurance vs Age

The below analysis examines death benefit for a preferred plus male at forty, fifty and sixty years old.

The above shows that after 40 years the cost for a 40 year old is 41 bps, 50 year old = 72 bps and the 60 y/o = 106 bps.

Tax Efficiency Illustrated

Assuming an investment turnover every few years with an effective tax rate of about 25%, a comparison with a 6% illustration might be insightful (8% x 75%.) Over 40 years, this strategic tax efficiency could yield a significant difference in returns—1.58% more, to be precise. This translates to a comparison of $10.5 million versus $6.1 million in accumulated value, showcasing the power of tax-advantaged growth in a VUL policy.

The other way to think about VUL is relative to a buy and hold strategy. In order to avoid estate taxes people move money into a trust and then buy equities in the trust. When it comes time for the beneficiary to access the capital they would sell the stock and pay capital gains. The average state + federal capital gains is ~35%. Using a VUL policy inside a trust is sometimes referred to as a “step up in basis” inside the trust.

In the below diagram the red line illustrates an investment ($100k for 7 years) compounding at 8%. The dashed red line represents what the tax adjusted value would be if the investment is sold. The blue dash line represents the death benefit value. The blue solid line is the cash value, which are the funds that can be borrowed against.

The moral of the story is that (in the case below) there is more cash value available relative to selling the traditional investment and there is a significant added benefit when the death benefit is realized.

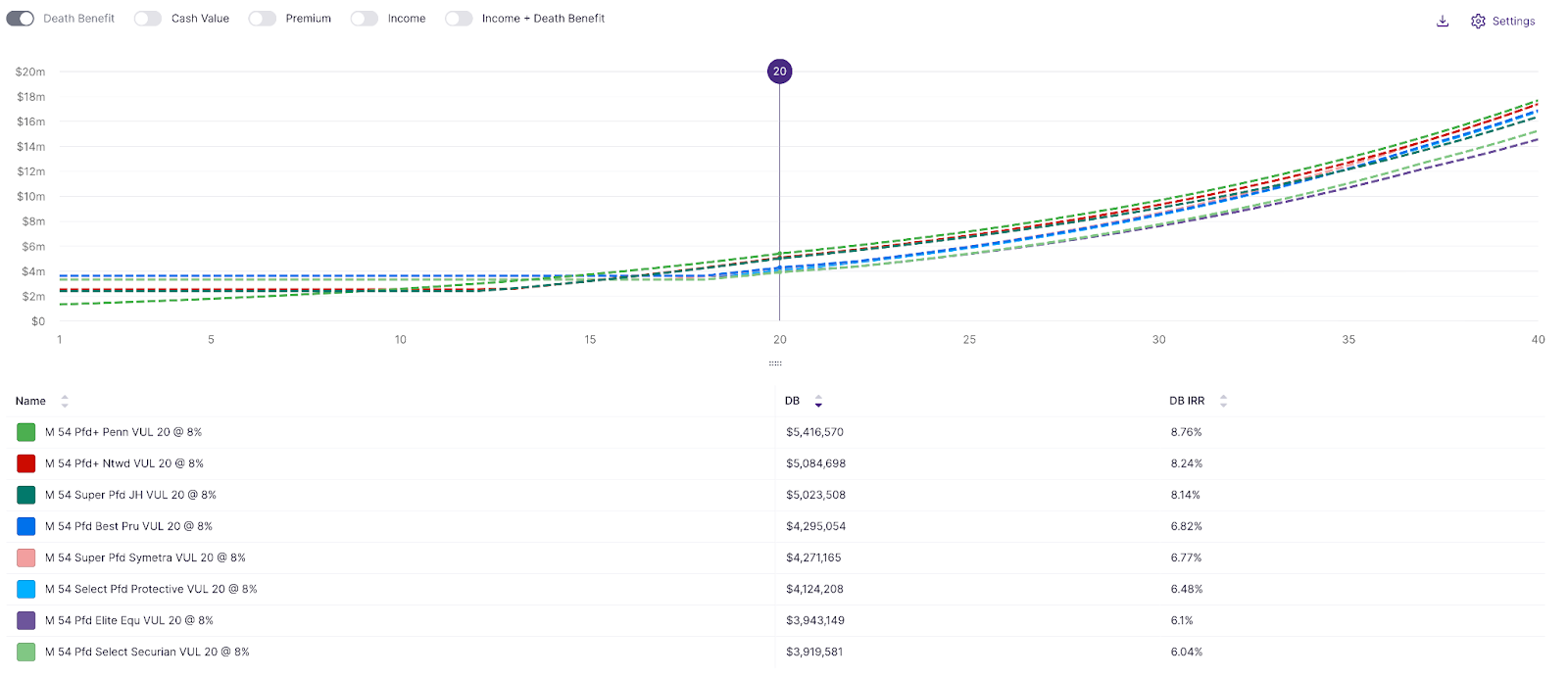

Carrier Variability

Notably, VUL policies are not one-size-fits-all. Different insurers may offer policies that start with a higher Death Benefit (DB) and experience slower growth, or they might cater specifically to certain ages, health statuses, and premium payment durations.

Take Action with Optifino

Navigating the complexities of VUL requires a keen understanding of its costs, benefits, and suitability to your financial landscape and goals. Optifino representatives can help provide expert guidance whether VUL is the right policy for you, helping you to optimize your assets and develop a plan tailored to your financial goals. We will also help you explore other policy options for wealth accumulation or wealth protection, explaining the merits of each product for contributing to your goals.