The “G” in GVUL

How Guaranteed Variable Universal Life Insurance Can Safeguard Your Future and Grow Your Wealth

How do you know if a GVUL policy is right for you?

The first step of the journey with Optifino begins with goal discovery, where we take the time to get to know the life stage and wealth priorities of a client. While most advisors or agents will ask for your goals and factor that into their recommendation, we built the technology to better identify the right policy based on their goals while removing any unconscious biases from the recommendation. By taking a more holistic approach to portfolio design, our Wealth Legacy Architects help propel your wealth goals forward, helping you move seamlessly through every life stage.

One of the first steps in the goal discovery process is understanding whether you are still building your wealth or whether you already have wealth. We call this the accumulation vs. protection question, in which there also is the option to take a “balanced” approach. One of the most often recommended policies for a balanced approach, as identified by our experts and AI, is a product called “GVUL” (Guaranteed Variable Universal Life). The G in GVUL means it provides a guaranteed death benefit. The Guaranteed Death Benefit can often be higher than other Guaranteed products like GUL, GIUL and the guaranteed portion of WL. This is due to the potentially lower reserves the carriers need to keep on their balance sheets with variable products.

GVUL policies also allow the policy holder to dictate how the funds the underlying capital is invested in. If the capital generates a >7-8% return the cash can grow to the point where the death benefit exceeds the guaranteed amount. This is a great product for estate planning and it also allows for greater cash accumulation that can be borrowed against tax-free—if it performs well. In these cases, the cash can be used for retirement, passion projects, really anything. With the underlying capital being allocated to uncapped equity linked products you have the potential to substantially outperform the guarantee. The choices for what to allocate the capital have been improving. For example, Penn Mutual recently announced an expanded Vanguard fund lineup for allocation choices.

The effect of the length of the Guarantee

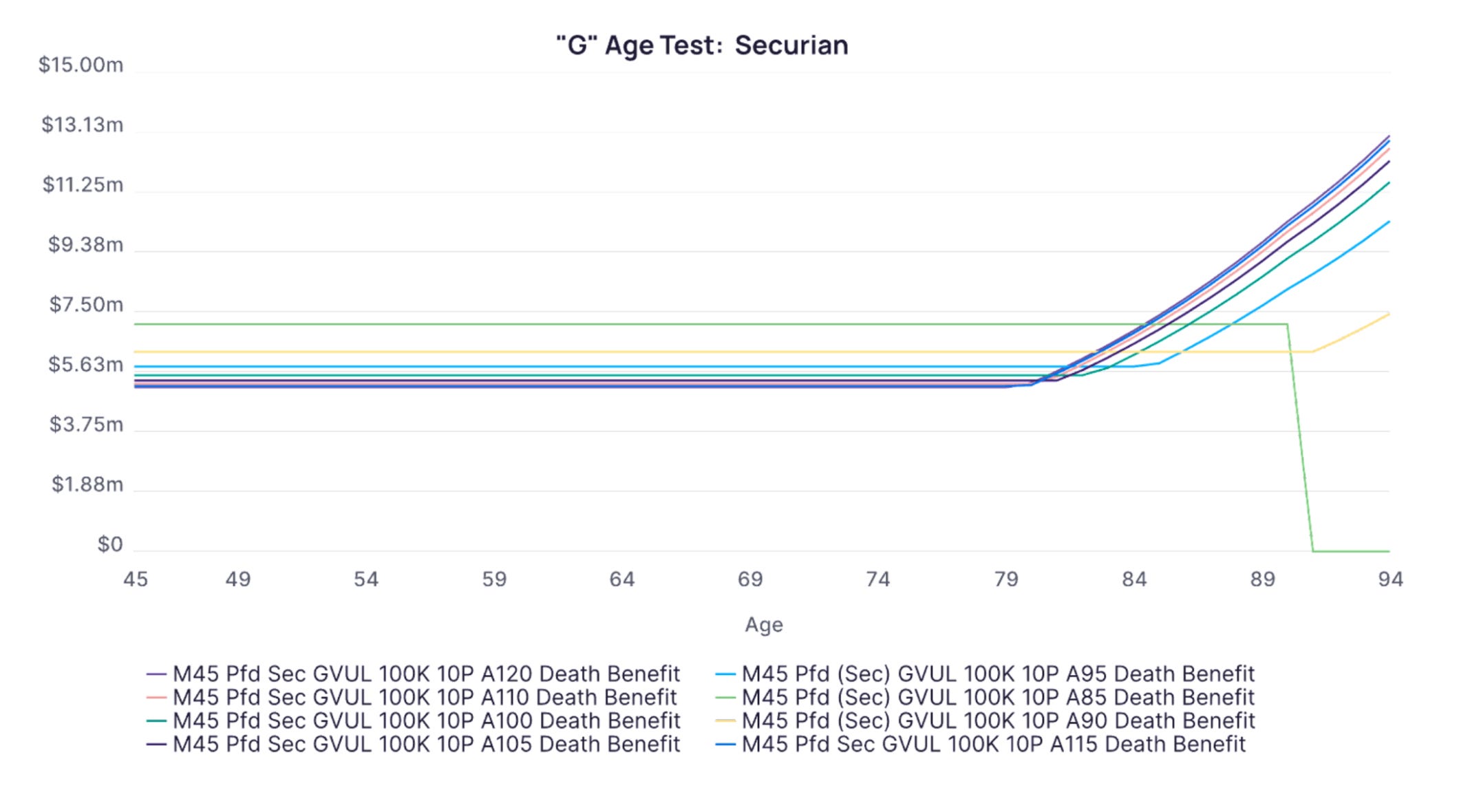

We are able to choose the length of the guarantee with all products that are approved on the platform. Usually, you can choose between age 85 all the way to age 121, and understanding the effect of this choice is paramount in optimal design.

Let’s look at a hypothetical client: Male, 45 years old, preferred health, GVUL, 10 pay @ 100k / year for 10 years.

The below graph compares the guaranteed death benefit of a GVUL policy from five top carriers at different lengths of guarantee.

These are our key observations based on the comparison:

We are always amazed at the dispersion of the carriers!

Generally speaking, the difference between age 100 and age 120 is negligible. So, if you are going to get a guarantee then go to 121! Can you imagine living to age 101 and then the policy lapses? … heart breaking! This is especially true if we are talking about policies on younger people that may actually live that long.

The Death Benefit substantially increases when you lower the guarantee to age 85 or 90.

Is the higher Death Benefit with a lower age guarantee worth it?

In order to understand the tradeoff, we need to start by understanding the concept of “NAR” (Net Amount at Risk). NAR is defined as the difference between the Cash Value and the Death Benefit of a policy. This is the amount of money the insurance company is on the hook for at any given time. The amount of money the insurance company is charging you on any given year is the “COI” (Cost of Insurance) is multiplied by the NAR. This means the tradeoffs of a higher guaranteed death benefit are:

Plus: A high guarantee is great because you feel peace of mind knowing your beneficiaries get a higher guaranteed death benefit.

Minus: A high guarantee creates a larger NAR, and this cost slows the cash build up.

The Securian product (below) demonstrates this very clearly. Here is the chart for the first 30 years of the policy.

The extreme example of a policy guaranteed to age 85 shows by far the best Death Benefit, but you can see how the cash grows much slower.

There are two major effects of the cash growth:

The faster the growth, the faster you have the chance to “break the corridor” (i.e. the cash value exceeds the guaranteed Death Benefit)

If the cash grows very high, substantially over the death benefit, you can safely withdraw or borrow capital

Let’s zoom in on the death benefit around the time the corridor breaks:

This is at an 8% gross return. What you see is the lowest guaranteed benefit (age 120) breaks the corridor first and then has the chance to have the highest ultimate death benefit.

To further visualize this here is just the Age 120 policy:

If the NAR is too much it will have a very large drag on the cash and can eventually cause the policy to lapse.

Here is a zoomed-out view of the cash values at an 8% gross return:

As you can see with the dashed light green above, representing a 10-pay GVUL policy guaranteed to 85, the cash value drops precipitously over the course of a few years. When the cash hits zero the policy will lapse (as seen by the below graph)!

When we look at a 5% gross case for all the carriers with an age 90 guarantee result becomes even scarier:

They all lapse!

Key Takeaway

If you want a guarantee, pay for it all the way to 121. The balanced approach provided by GVUL policies creates substantial potential upside while promising protection. Actual performance will vary based on how the underlying capital is allocated and based on the terms offered across carriers based on your profile. Each carrier will tailor the fine print—that impacts policy performance differently—based on your demographics and budget needs so carriers do not always perform in the ranking as illustrated in the examples above. We can help you quickly understand your potential outcomes based on your goals, and, if you already have one, compare your current policy with one more aligned with your goals.