Should I Convert My Convertible Term Policy?

A Case Study On Why Sometimes Letting Convertible Term Lapse is the Best, Most Optimal Strategy

Many policyholders face a crucial decision when their convertible term life insurance policies approach their conversion date. The conventional wisdom is to convert these policies to preserve favorable health ratings and lower insurance costs. However, a recent case we consulted on reveals that converting the convertible term policy may not always be the most cost-effective strategy. Since carrier costs can vary as much as 60% for the same product and each carrier has their own strengths, we found that converting the policy with the same carrier would result in higher premiums for the same death benefit.

The Case Study

We recently met with a 60-year-old client with multiple convertible term policies nearing their conversion dates. The client had previously consulted a broker who recommended converting all policies, without considering the broader marketplace nor the client's present health status. Unfortunately, most agents and advisors lack the tools to properly compare the entire marketplace—the reason our platform is so powerful—so this is the conventional approach and it has negatively impacted conventional wisdom.

The Conventional Approach

The previous broker's strategy involved:

Assuming the client's health status remained unchanged

Converting policies to preserve the original preferred-plus rating

Failing to compare options across the top carriers

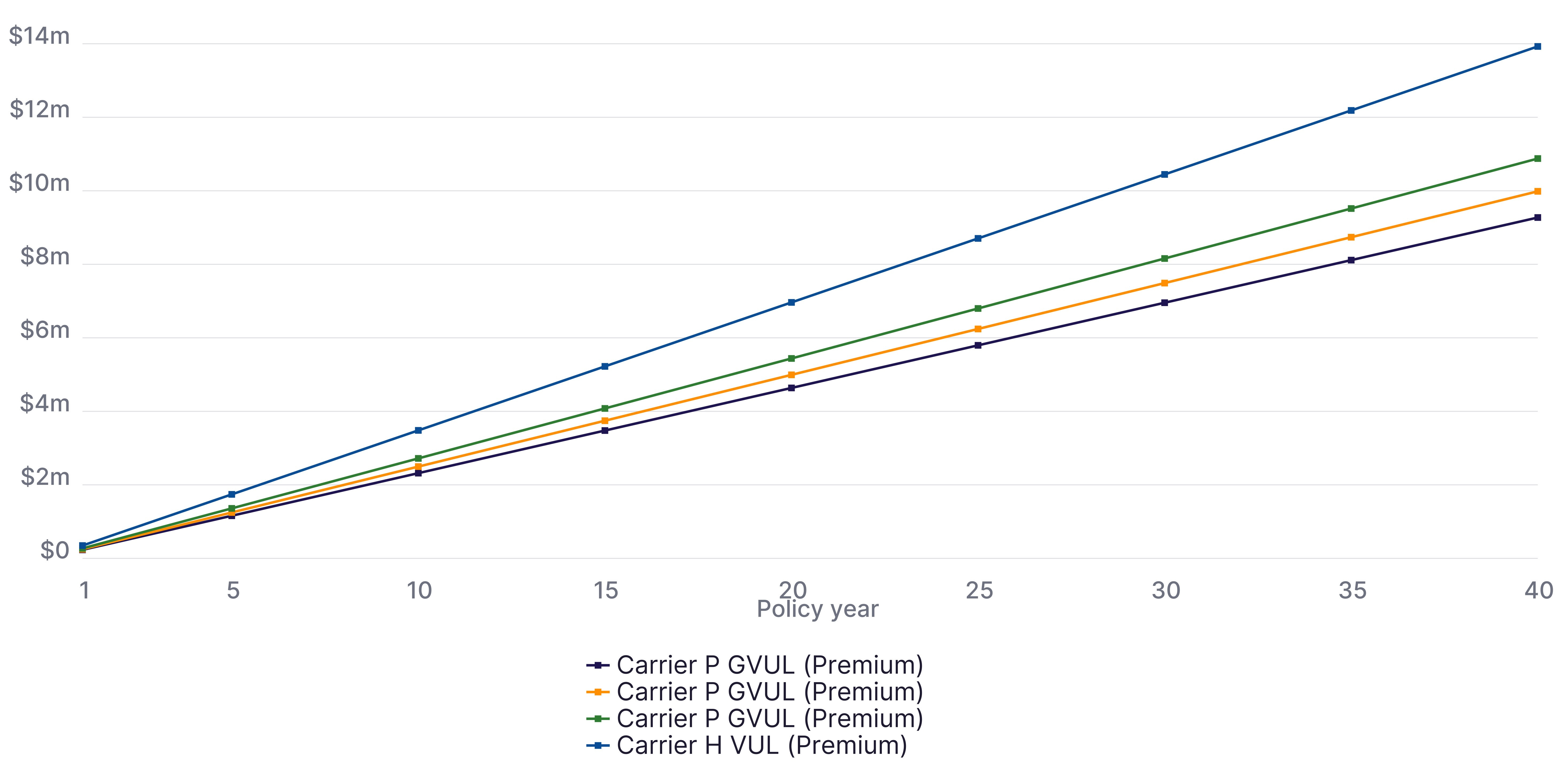

This approach led to a significant policy conversion, with a $10 million face value and an annual premium of approximately $200,000.

The Problem with Conventional Wisdom

Several issues arose from this conventional approach:

The chosen carrier specialized in accumulation-type policies rather than protection-focused policies.

The client's wealth status dictated a need for protection-focused coverage.

The broker failed to conduct a thorough discovery process or market comparison.

The Optifino Approach: Always Canvas the Market

At Optifino, we believe in thoroughly evaluating all options before making a decision, which is why we built the platform to be able to do so in minutes. Our philosophy involves:

Canvassing the entire marketplace for each policy decision

Utilizing our advanced comparison engine for efficient market analysis

Considering the client's current health status and financial goals

Showcasing the options and potential outcomes in an easy visualization

Our Findings

Upon analyzing the market, we discovered:

Protection policies from other carriers offered significantly higher death benefits (for the same premium) or lower premiums (for the same death benefit).

The client could potentially save approximately 40% on premiums (paying $120,000 annually instead of $200,000).

Even if the client's health status had dropped to standard, they could still save 30% on premiums.

Key Takeaways

Don't assume conversion is always the best option: While converting a policy can preserve a favorable health rating, it may not result in the most cost-effective solution.

Regularly reassess your insurance needs: As your financial situation changes, so should your insurance strategy that is why we are setting an industry gold-standard of annual reviews.

Consider the ever-evolving marketplace: Insurance carriers are always introducing new product innovations, and new products may provide better value than converting an existing policy.

Update your health status: A current health assessment can open up new, potentially more favorable options.

Work with an advisor who compares the entire market: A thorough market analysis can reveal significant savings opportunities.

Closing Thoughts

By challenging conventional wisdom and taking a data-driven approach to policy decisions, policyholders can potentially save millions of dollars over the life of their insurance coverage. While this case study represents a client with substantial wealth and a larger budget than most of us, the lesson applies no matter your wealth level. Always consider canvassing the market and updating your health status before automatically converting a term policy, even if it is just for the peace of mind of knowing you did your due diligence.