Safeguarding Your Retirement Against Economic Volatility

Discover the Dual Benefits of Life Insurance in Retirement Planning and Wealth Management

With persistent inflation and the S&P close to all-time highs, many people expect market volatility ahead. While permanent life insurance is often thought of only in terms of its death benefit, it also can be a yield-generating cornerstone of a portfolio that hedges against volatility. With the recent CPI report showing consumer prices rose 3.5% from a year ago in March and uncertainty around how long the S&P can continue this performance, timing the market could prove more difficult than ever. In this scenario, a holistic financial strategy that creates tax-advantaged access when you need it is especially important, and offers a powerful financial vehicle in retirement planning. Both advisors and policyholders can benefit from a greater understanding around the power of life insurance in retirement planning.

Hedge Against Volatility

Permanent life insurance offers a unique combination of growth potential and stability. It offers policyholders greater control over their financial destiny, allowing for flexible premium payments, the ability to optimize towards better performing life insurance products, and access to cash values that can serve as a financial safety net or liquidity to invest in opportunities. When advisors are able to tailor life insurance policies—factoring in life stage, income-affluence, and goals—policyholders have a greater understanding of how their life insurance policy will work towards their goals. The growth of cash value within many permanent life insurance policies can often increase more quickly than inflation, providing a potential hedge. The cash value can then be accessed without paying capital gains or income tax.

Planning for Retirement

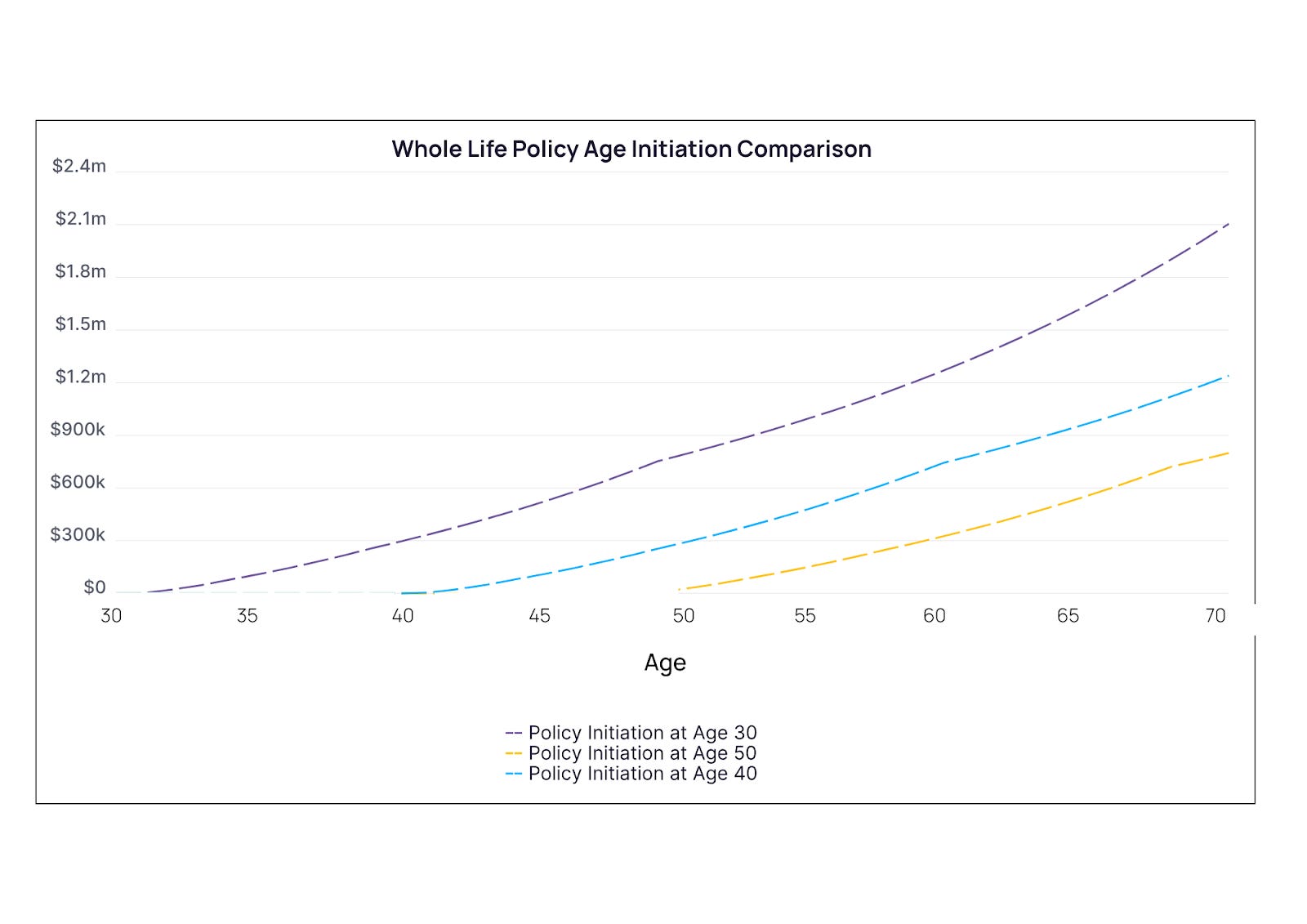

According to a new report from Northwestern Mutual, Americans now believe they need $1.46 million to retire comfortably — a jump of 53% from their savings target in 2020. Whether this is driven by Americans wanting to spend more in retirement or concerns over inflation, life insurance is too frequently overlooked by people as an effective asset for creating a holistic retirement plan. When tailored for your goals and aligned with your broader portfolio, the cash value can provide accessible, supplemental retirement income when needed. Take the below example: where we assume the client contributes $10k in premiums to a Whole Life policy per year for 10 years starting at different ages.

If we’re assuming that $1.46 million allows for a comfortable retirement and that the cash value grows at an 8% return, then we can get pretty close to that amount if we initiate the policy at forty years old (and easily surpass that mark when initiated at thirty). While this projection is based on a Whole Life policy, the spectrum of life insurance policies create a plethora of approaches to embracing growth, protection, and risk. The policy attributes that a policyholder needs to prioritize changes based on life stage and wealth, so it’s imperative that a policy is reviewed annually to ensure it stays on track of the projected outcome. If not, the ability to transfer your policy to a better performing product with a 1035 exchange can help insulate from uncertainty and volatility.

While policy performance is ultimately dependent on the performance of the carrier and the fine print of your policy, the takeaway is clear: permanent life insurance creates peace of mind for those who want to be comfortable and pursue their passions in retirement. This all begs the question. How do you avoid the hidden dangers of the fine print and keep track of policy performance against your goals?

Fine Print & The Importance of the Annual Professional Review

The reason for all the fine print is not for any nefarious reason, but because the carriers introduce thousands of product iterations across 10+ types of life insurance product types. In other words, they constantly introduce new product innovations to capture new niches of the market and insulate themselves against market volatility. This means that the fine print can vary widely from policy to policy, and carrier to carrier, based on your risk profile. Keeping up with how the fine print affects policy performance, in addition to the constant product innovations, is too much for any one person to handle—policyholder or advisor.

We can help you (or you and your client) unlock the strategic power of permanent life insurance in retirement planning, and we continue to work with you to optimize your policy against your goals when they evolve. We will identify the best policy out of hundreds of thousands of potential outcomes based on your life stage, risk appetite, and desired premiums—propelling your growth and one step closer to the retirement you deserve. Tailored permanent life insurance stands as a resilient solution for individuals looking to build and protect their wealth amidst economic uncertainty, and we at Optifino will ensure you feel comfortable navigating it.