Permanent Life Insurance, What’s The Point?

Understanding Why The Wealthy Store So Much Wealth In Cash Value Life Insurance

If you want the easy answer: Life Insurance is largely utilized for the living benefits, in addition to the death benefit, because its one of the last tax-advantaged assets.

While there are thousands of different types of policies across dozens of top carriers, and each one of those types of policies have unique benefits, they all offer varying degrees of wealth accumulation or protection, risk exposure, and payment durations. Many people ask what policy type is best, however there is only the right type of policy that is best for your goals and life stage.

Before we get into explaining the many different policy types, it’s important we establish the basics. Section 101 of the IRS tax code excludes the death benefit from a life insurance contact in gross income. This means you can compound money tax free over the life of the policy and the beneficiary receives the final amount tax free. i.e., you avoid capital gains tax.

To demonstrate the power of this we can examine two of the carrier’s products: Whole Life (WL) and Variable Universal Life (VUL).

Variable Universal Life (VUL)

Essentially this product “wraps” an underlying asset in an insurance policy. The monies sit in a separate account—not on the carrier’s balance sheet. You have the ability to pick from dozens of indexes and ETFs in which to invest the cash value, and you can change your mind as often as you want. The tax implications are straight forward. Here is an example comparing cash value growth in a VUL policy versus investing the same amount of money and paying capital gains:

As you can see, over a longer time horizon the impact of capital gains decreases, but for people with shorter time horizons, the power of VUL is evident. If you’re younger—say 30 years old—then VUL may not make as much sense, but the older you get, the more valuable VUL becomes.

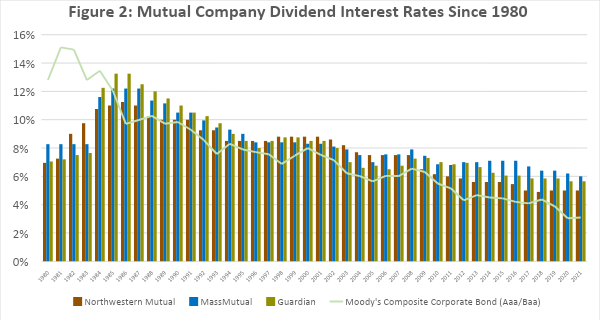

Whole Life (WL)

In a WL product the money you pay (premiums) is held on the carrier’s balance sheet. The carrier invests the money and you receive a dividend, which usually involves a guaranteed minimum. What you see is that the dividends essentially correlate to the Moody’s bond index.

Again, the difference (or the arbitrage) is that the dividends you get (or yield) is tax-differed and eventually tax free. If you need access to the cash value, you can borrow against the policy at very competitive rates—often 1-2 percentage points higher than the guaranteed IRR.

That’s really the whole game: minimize tax-liability in your lifetime and for your beneficiaries. There are many nuanced products that we can walk you through but understanding this core principle and that the best policy for you must is a function of your financial goals is key to getting started. That is why we built a first-of-its-kind platform to integrate your financial goals with policy design, and continue to provide annual policy reviews as your goals evolve.

Stay tuned for our next post talking about the spectrum of life insurance products. Drop any questions you want answered in the comments!