Creating Generational Wealth with IUL and VUL Policies

A Case Study on How Combining Strategies Can Build a Family Legacy

Building generational wealth requires a thoughtful approach—balancing market exposure, risk management, and long-term security. Recently, we worked with a client couple who, having already accumulated a substantial wealth portfolio, wanted to establish a meaningful legacy for their children. They wanted to be able to tap into the market for themselves, since they had the time to lean into more risk, while also laying a strong financial foundation for their children’s future. Their goal was to create a financial framework that would offer flexibility, tax-advantaged growth, potential upside with market exposure, and security for their family’s future. After taking the time to understand their goals, we developed a tailored plan that combined two Indexed Universal Life (IUL) policies on the parents and two Variable Universal Life (VUL) policies on the children.

Background: Crafting a Personalized Plan

Let’s call them the Barrys. The Barrys, a 40-year-old husband and a 36-year-old wife, came to us seeking to diversify their financial strategy and develop a more holistic portfolio outside of their investment portfolio—one that offered more than just the catastrophic protection their previous term policy provided. Given their relatively young age and their expectation to work many more years, the clients had time to take on moderate risk, allowing their investments to compound over the long term.

With a significant investment portfolio, their goals were:

Introduce greater flexibility and long-term security

Mitigate risks while maintaining exposure to market growth

Create a tax-advantaged foundation that would build generational wealth

The Solution: Balancing Risk and Reward

After evaluating their needs, we recommended a portfolio of policies that would create flexibility for them and build tax-advantaged wealth for their annual budget of $50k.

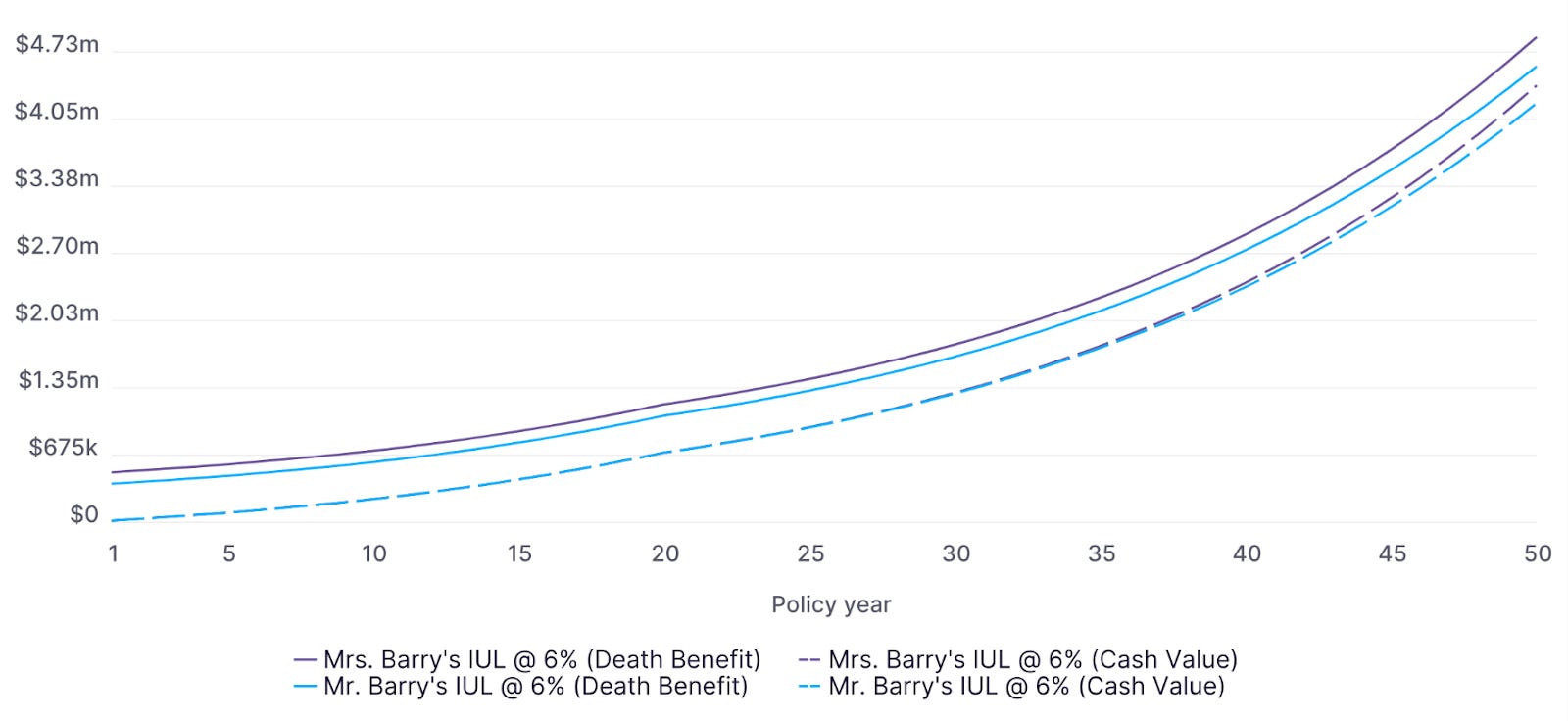

The two 20-Pay IUL Policies on the parents offered market exposure and a reliable pathway for growth, with the flexibility to convert into a policy with a guarantee later in life—when their goals were more conservative.

Policies on the Parents

Annual Premium: $40,000 (combined).

Initial Death Benefit: $2.6M (assuming a 6% return).

Projected Cash Value at Age 65: $3M (assuming a 6% return).

Projected Death Benefit at Life Expectancy: $8.6M (assuming a 6% return).

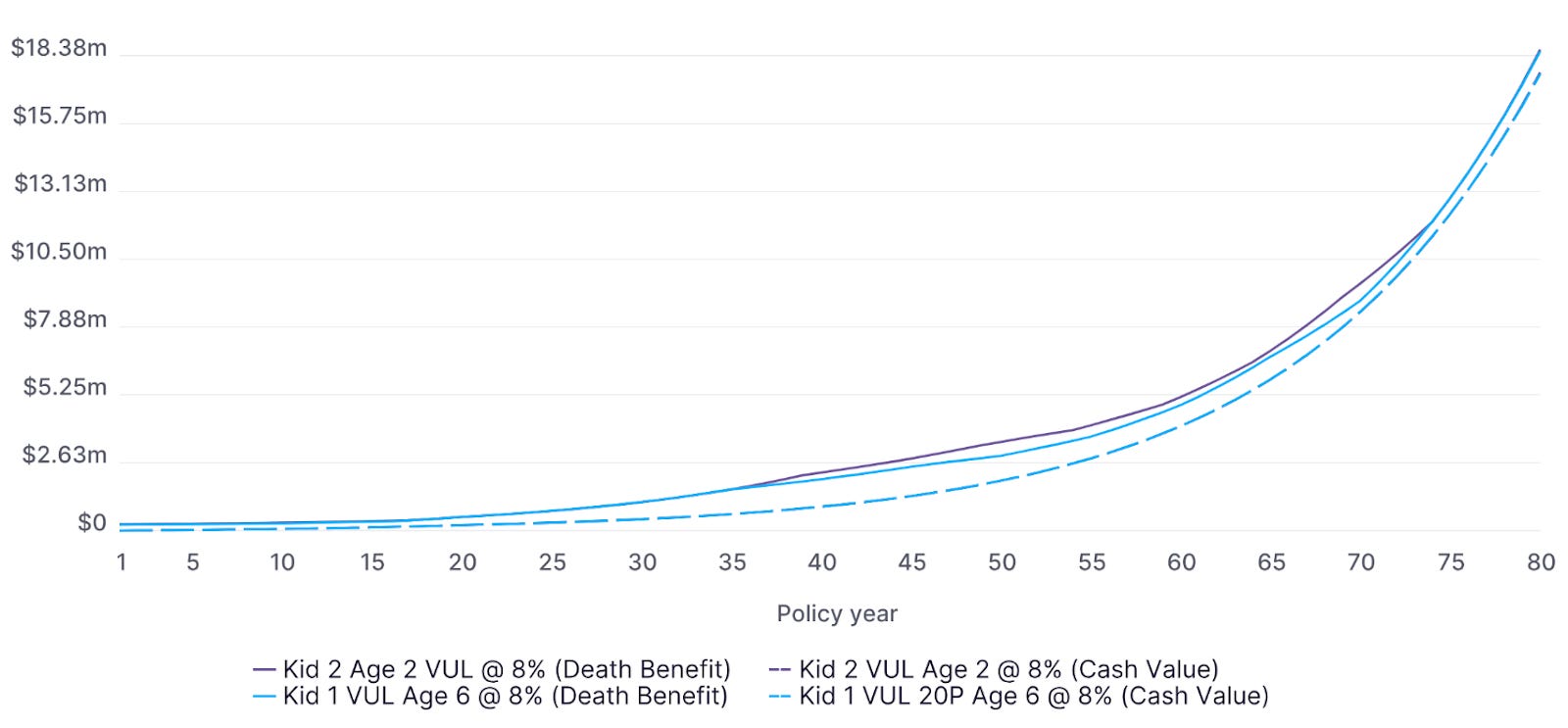

The two 20-Pay VUL Policies on the Children were tailored for longer-term growth and substantial potential upside. Taking out policies on their young children capitalized on the low cost of insuring children of that age so that by the time they were adults, there would be a substantial tax-advantaged pool of wealth they could access tax-free. They could choose to use the funds to purchase their first house, start a business, or simply have the peace of mind that they were already protected when they themselves decided to have children of their own.

Policies on the Children

Annual Premium: $10,000 (combined).

Initial Death Benefit: $461K (assuming an 8% return).

Projected Cash Value at Age 65: $8.8M (assuming an 8% return).

Projected Death Benefit at Life Expectancy: $28M (assuming an 8% return).

Closing Thoughts

The Barry's policy portfolio demonstrates the power of a personalized financial strategy that can only be created by canvassing the marketplace across top carriers. The ability to quickly and easily illustrate the combined potential outcomes of the policy portfolio simplified the decision for the Barrys. By combining IUL and VUL policies, our clients were able to achieve financial benefits for themselves while laying the foundation for their children—even the next generation if appropriately managed. At Optifino, we pride ourselves on crafting personalized plans tailored to each client’s unique needs and goals. Whether you’re looking to protect your family’s future, build generational wealth, or explore market opportunities, we can help you find the optimal solution in minutes.